‘The BUBA is in” was a common refrain that market fossils (myself included) can recall from the halcyon era of successful central bank intervention in the foreign exchange (FX) market in the mid- to late 1980s.

This communication, from inter-dealer brokers to FX dealers across the globe, indicated the presence of the German Central Bank (Bundesbank) in the market, often acting “in concert” (in unison) with other major central banks, to influence the US dollar exchange rate against key currencies, such as the Deutsche Mark, Japanese yen and Swiss franc.

FX dealers, in banks and other institutions, would frantically “cut” (close), or even reverse, speculative positions, as their Reuters screens would typically announce: “Bundesbank, Bank of France, Federal Reserve, Bank of Japan, Bank of England (etc.), all sell dollars.”

The first notable example of such concerted intervention was indeed to weaken the US dollar, following its stratospheric rise in the early 1980s. This rise was largely a result of the restrictive monetary policy of the US authorities, which resulted in dollar interest rates rising to record levels and thereby attracting huge capital flows into the currency, to the detriment of others (sound familiar?). Indeed, from 1980 to 1985, the dollar had appreciated by 50% against the Deutsche Mark and other leading currencies, and fears grew of the adverse impact such dollar strength was having on an already burgeoning US trade deficit.

The Plaza Accord of 1985

In an impressive show of unity, the Plaza Accord of 1985 was signed by the finance ministers and central bank governors of the G5 (France, Germany, US, UK and Japan) in Manhattan’s Plaza Hotel, with the signatories all agreeing that “some orderly appreciation of the non-dollar currencies is desirable (…) and we stand ready to cooperate more closely to encourage this, when to do so would be helpful”.

No sooner was the ink on the accord (and the hotel bar) dry, when a period of “concerted” central bank intervention in the FX market ensued, with frequent orders being given to FX dealers in banks across the world to execute the sale of billions of US dollars into the market, in an effort to weaken the currency.

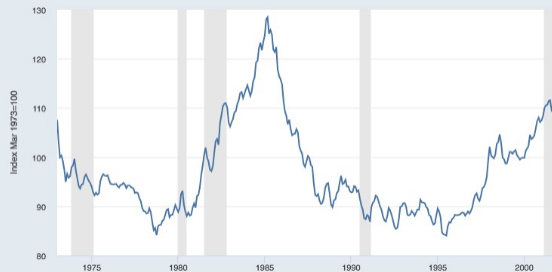

As can be seen in the chart of the US Dollar Trade-Weighted Index below (based on the value of the buck against the currencies of its trading partners), these actions were certainly very successful in reversing the trend; in fact, so successful that a subsequent agreement, the Louvre Accord, was required in 1987 to stem the slide in the value of the US dollar, which by that time had lost more than 50% of its value since Plaza.

Source: St Louis Fed

But intervention had its limits and, 30 years ago this month, on “Black Wednesday”, the UK pound was knocked out of the European Exchange Rate Mechanism, which was designed to stabilise a number of European currencies, as the Bank of England’s intervention failed to thwart a speculative attack.

Those events underlined the rise of “hedge funds” as speculative forces to be reckoned with, and George Soros’s infamous Quantum was simply one of many. Having only really appeared as significant market participants a few years previously, it seemed that these “alternative investment” entities could already confound efforts by monetary authorities to defend their exchange rates. The cheek of it!

While there are many different forms and “styles” (techniques used) of hedge funds, many of the so-called Macro funds specifically target exchange rates for speculative purposes, using derivative instruments and other techniques to “leverage” (amplify) their investors’ capital into market bets, which can be for multiples of the actual assets under management (AUM). When one considers that the Top 25 macro funds alone had a combined AUM of $685-billion in 2021, according to HedgeLists.com, it is clear that these alternative investment intermediaries can certainly pack a punch.

Indeed, only a few years later, in 1997, the hegemony of the fast-growing hedge funds in the foreign exchange markets was vividly displayed, when speculative forces combined to force a number of Southeast Asian countries to allow their currencies to devalue, often sharply; the Indonesian rupiah lost 80% of its value in a few months.

1998 Russian default

The following year, 1998, witnessed a completely unexpected and irrational decision by the Russian government (oh, really!), when it decided to default on repayment of local currency-denominated bonds (debt). This petulant decision sent shockwaves through the financial markets, leading to unprecedented global exchange rate volatility and sharp devaluations of many emerging market currencies, including the South African rand.

The events of 1998 prompted the South African Reserve Bank to abandon its long-standing policy of defending the rand, via periodic direct sales of US dollars into the market, a policy that had in fact been quite successful in terms of protecting the actual exchange rate, but which had proved to be damaging to the wider economy and fiscus.

Fast-forward to 2022 and it is clear once again that rapidly increasing US dollar interest rates have contributed to huge currency market instability, as can be seen below in a chart of the US Dollar Trade-Weighted Index for 2022. For example, the US dollar exchange rate against the Japanese yen has appreciated from 115.00 yen per dollar, at the beginning of the year, to almost 145.00 at the time of writing. Similarly, the British pound has recently fallen to a record low against the rampant dollar, and the euro has fallen through “parity” (1-for-1) against the greenback, for the first time in 20 years.

Source: St Louis Fed

Among the consequences of a stronger dollar is the inflationary impact it has for countries that rely on imports of dollar-priced goods, such as oil and essential foodstuffs. A stronger dollar is also usually negative for the balance of payments of many countries, since these dollar-denominated imports are simply more expensive to purchase.

So, if US dollar strength is a problem, and in the absence of an alternative plan, why not try a bit of good old-fashioned “eyebrow-raising” by central bank governors when meeting with major FX dealing institutions, backed up with a concerted initiative to flood the FX market with huge sales of US dollars? In addition, throw in some form of regulatory restriction on the activities of speculators, from limitations on permissible leverage, through to outright banning of certain types of market participation.

Visit Daily Maverick’s home page for more news, analysis and investigations

A recent opinion piece by Richard Cookson, “Coordinated Dollar Intervention is a Long Shot”, identifies some reasons that, notwithstanding the current concerns of many countries, the top central banks “are unlikely to team up to arrest the US currency’s strength”.

Cookson’s reasons focus on the differing policy priorities among the major players, which would seem to undermine any attempt at reaching consensus on the objectives and even desirability of such actions. First and foremost, he argues that most of the countries that are complaining about weakening currencies, at present, are guilty of self-inflicted injury, due to their deliberately lagging behind with local interest rate increases, which would reduce the relative yield advantage of US dollar deposits.

Cookson also proposes a somewhat more sinister hypothesis for the current inaction, insofar as he suggests that the stronger US dollar may, in fact, be a deliberate policy weapon being deployed by the US administration against long-standing economic foes (read: China).

The modern FX market

Perhaps, however, there is another and less conspiratorial reason that most central banks no longer choose the intervention option: the modern FX market, and the huge speculative forces lurking there, might simply swallow them up, belch and move on. This market has grown to a staggering $6.6-trillion of turnover on average per day, according to the latest figures published by the Bank for International Settlements (BIS), which challenges in a couple of days the total FX reserves of all of the world’s central banks, which currently stand at $12.5-trillion by IMF estimates.

Interestingly, figures from the BIS show that the majority of global FX market activity is undertaken by “non-bank financial institutions”, which includes alternative and traditional investors, who collectively command serious firepower, and who are definitely not shy in moving their investments around in search of yield. Attempts to restrict the activities and choices of these institutions could, themselves, lead to even more damaging consequences and market instability.

As unlikely and unwise as it may be, therefore, for a return to the old days of central banks engaging in direct FX market intervention, stranger things have happened in recent economic history. Indeed, it is worth recalling that, only a few years ago, the Swiss National Bank, acting alone, successfully, if only temporarily, halted an unwelcome strengthening of the Swiss franc against the euro, in the face of significant speculative forces.

Similarly, the Bank of Japan has itself recently and bravely “taken on the market”, by intervening to stop the yen’s precipitous slide, an initiative that seems to have taken the wind out of the sails of the yen “bears”, if only for now.

If the key economic decision-makers of the world do, in fact, decide to go for it in full force, however, one can only imagine the facial expression of the foreign exchange trader rushing to answer the characteristic “direct (telephone) line” from the central bank, when the solemn voice on the other end utters the soon-to-be immortal words: “EUR/USD in a Trillion, Please.” DM/BM

Comments - Please login in order to comment.